Notification of Cessation of Employment

Cessation of employment / termination of employment / cessation due to death:

- If the employer will cease employing an employee who:

- is subject to tax in respect of employment income; or

- is likely to be subject to tax in respect of employment income; or

- an employee under employment dies, the employer is required to submit Form CP22A / CP22B not less than 30 days before the cessation of employment or not more than 30 days after being informed of the death.

- Mulai 1 Januari 2024, Borang CP22A / CP22B wajib dikemukakan secara dalam talian melalui portal MyTax menggunakan aplikasi e-SPC. Manual Pengguna bagi e-SPC boleh dicapai melalui Mytax > Panduan Pengguna. Majikan juga boleh merujuk kepada Manual Penggunaan Permohonan Peranan dan FAQ MyTax yang boleh dicapai melalui MyTax > Panduan Pengguna bagi memudahkan penggunaan aplikasi e-SPC.

- However, employers are not required to submit the said form if an employee’s income is subject to Monthly Tax Deduction (MTD) or if the employee’s monthly remuneration is below the minimum amount eligible for MTD.

- Any employee who is not subject to the exemption under paragraph 3 above, the employer is required to withhold any money payable to an employee who has ceased or will cease employment. The employer must also not pay such money to or for the benefit of the employee without permission from HASiL until 90 days after the receipt of Form CP22A / CP22B by HASiL

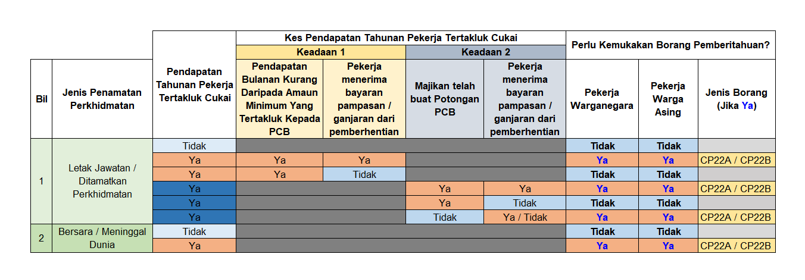

- The table below serves as a general guide for employers in determining the requirement to submit the CP22A / CP22B notification form. Based on the table, employers are required to submit Form CP22A / CP22B through e-SPC only for cases subject to the SPC requirement.

- Employers and employees may refer to Guidelines on the Procedure for Applying for an Individual Tax Clearance Letter (SPC). (345.35 KB) to gain a better understanding in carrying out their responsibilities more effectively.

Leaving Malaysia for more than 3 months:

- If an employee who is subject to tax in respect of employment income leaves or intends to leave Malaysia for a period exceeding 3 months, the employer is required to submit Form CP21 not less than 30 days before the employee’s expected departure date.

- Starting from 1 January 2024, Form CP21 must be submitted online through the MyTax portal using the e-SPC application

- However, the employer is not required to submit the said form if the Director General of Inland Revenue is satisfied that the employee is required to leave Malaysia frequently in connection with his employment.

- Employers are required to withhold any money payable to an employee who leaves or intends to leave Malaysia for a period exceeding 3 months without the intention to return. Employers must also not pay such money to or for the benefit of the employee without permission from HASiL until 90 days after the receipt of Form CP21 by HASiL

- The table below serves as a general guide for determining the requirement to submit the CP21 notification form:

| Employee Scenario |

Employee Annual Income – Subject to Tax |

Is Submission of Notification Form Required? |

Type of Notification (If Yes) |

| Leaving Malaysia for More Than 3 Months |

No |

No |

|

| Yes |

Yes |

CP21 |

Non-compliance by employers

- Failure to comply with these obligations without reasonable excuse, upon conviction of the offence, shall be liable to a fine of not less than RM200 and not more than RM20,000, or imprisonment for a term not exceeding 6 months, or both.

- Employers are responsible for paying the full amount of tax payable by their employees. The amount payable by the employer constitutes a debt due to the Government and may be recovered through civil action.

Relevant provisions:

- Subsections 83(3), (4) and (5) of the Income Tax Act 1967

- Subsection 106 of the Income Tax Act 1967

- Subsection 107(4) of the Income Tax Act 1967

- Subsection 120(1) of the Income Tax Act 1967